Basics of Financial Markets

Published by Jainam Broking Limited — Prosperity with Security

Copyright Notice

Recipients of this book should note that the contents are only for the purpose of imparting knowledge and awareness on Financial Markets.

Copyrights and all rights of reproduction and translation are reserved by Jainam Broking Limited. No part of this book or publication may be reproduced in any manner including photocopying or storing by electronic means, or translated in any other language, without written permission of the copyright holder.

Due care and diligence has been taken while editing and printing the book; neither the author nor the copyright holder or publisher holds any responsibility for any mistakes that may have inadvertently crept in.

Disclaimer: The matter contained in this text is not to be construed as financial advice. Readers who wish to consider the material for investment purposes are advised to seek competent professional help. Recipients of this book should note that the contents are only for the purpose of imparting knowledge and awareness on Financial Markets.

Foreword

The evolution of India's financial markets over the past decade has been nothing short of transformative. With rapid digitalisation, stronger regulatory frameworks, and a more informed investor base, the financial ecosystem has become vibrant, inclusive, and globally connected. In today's environment, financial literacy is no longer optional — it is essential for anyone aiming to build a secure and prosperous future.

Basics of Financial Markets arrives at a crucial time when structured, accessible, and credible financial knowledge is needed more than ever. This book acts as a simplified and comprehensive guide for beginners, young investors, students, and professionals seeking to understand the foundations of market operations. It breaks down complex concepts into clear, practical insights, helping readers navigate the financial landscape with confidence.

What sets this initiative apart is its commitment to making financial education approachable. In a world where information is abundant yet often confusing, such clarity becomes invaluable. The book promotes disciplined learning, informed decision-making, and responsible market participation — qualities essential for sustainable wealth creation.

At Jainam, we have always believed that knowledge is the strongest asset an investor can possess. By empowering individuals with financial awareness, we not only contribute to their personal growth but also to the nation's economic progress. I am confident that this book will inspire readers to begin or strengthen their journey toward becoming informed and capable market participants.

I congratulate the entire team involved in bringing this book to life and extend my best wishes to every reader embarking on this journey of financial learning.

Preface

The Indian financial market is one of the oldest and most dynamic markets among emerging economies. Over the past few years, it has undergone a remarkable transformation driven by structural reforms, rapid technological advancements, and a steadily growing base of informed investors. Backed by strong regulatory oversight and sound economic fundamentals, India's financial ecosystem today plays an increasingly important role not only in domestic economic progress but also in influencing global investment flows.

In the wake of recent global disruptions — from the COVID-19 pandemic to inflationary pressures, supply chain shifts, and geopolitical realignments — the need for strong financial literacy has become more critical than ever before. As India continues its trajectory as one of the world's fastest-growing major economies, investors need to understand how financial markets operate and the vital role they play in enabling long-term wealth creation.

This book, Basics of Financial Markets, has been created for readers who wish to build a solid foundation in the financial market. It guides beginners through the essential principles, structures, and mechanisms that drive market functioning, presented in a simplified and lucid manner. The objective is to help readers navigate the complexities of the financial system with greater clarity, awareness, and confidence.

At Jainam, our constant endeavour is to demystify finance and make market knowledge accessible to everyone — especially young and aspiring investors. Through this book, we aim to inspire individuals to begin their journey toward becoming informed, responsible, and empowered participants in the financial markets. As we continue to evolve along with the market, we firmly believe in the timeless wisdom:

Every effort has been made to ensure that the content is clear, concise, and accurate. However, we recognise that continuous improvement is a part of growth. We sincerely welcome constructive feedback and suggestions from our readers.

You may write to us at: rajiv.singh@jainam.in

Table of Contents

- Introduction to Investments 01

- Financial Markets 11

- Risks Involved in Financial Markets 21

- Primary Market 26

- Secondary Market 44

- Market Intermediaries 53

- Depository Participants 59

- Factors Affecting Market 70

- Investment Products Available in Market 79

- Why Invest in Equity? 87

- Equity Market 95

- Corporate Actions 112

- Derivatives 121

- Mutual Funds 140

- Analyzing Financials of a Company 150

- Ratio Analysis 166

- Financial Planning 176

- Why Jainam? 189

Chapter // 01

Introduction to Investments

Why Should One Invest?

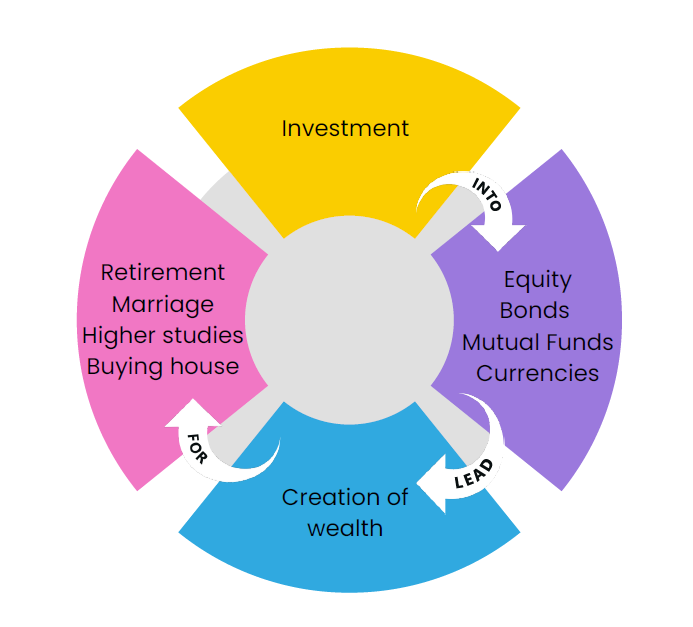

The answer to this question is to create wealth which eventually helps individuals to fulfil their financial goals for future needs. So, what is investing and how does it help individuals in creating wealth? Investment is defined as an asset or item that is procured in anticipation that it will generate returns or capital appreciation in the future. Many people talk about investing their money in certain asset classes in order to meet their financial objectives. The investment can either be done in fixed deposits, equities, gold, or even real estate. Among all asset classes, fixed deposit is the most widely invested asset class among investors. That's mainly because of its risk-free nature and it also gives fixed interest returns as interest to its investors. But in the current scenario, mere savings in fixed deposits may not be sufficient for an individual to meet long-term goals.

The lifestyle, necessities, and standard of living of people have evolved with the passage of time. So in order to meet all the requirements, it has become very essential to plan an alternative investment plan accordingly. Most individuals are dependent on a single source of income while their needs span immediate, medium, and long-term horizons. As Warren Buffet said:

— Warren Buffet

For instance, When one moves from one goal to another with current accumulated savings, minimal savings are left for long-term goals. Hence, it is important to not only keep money in a savings bank account, but also invest in asset classes that help create wealth over a long period of time.

One of the golden rules of investing says: if investment is started early, one might be in for a surprise in the later years. It's all because of the compounding factor — often called the eighth wonder of the world because of its power to multiply money over a period of time.

Case Study

Pranav and Rohit are friends, both are 30 year old. Pranav invests Rs. 1,000 every month for his retirement and gets an annual return of 12% on his investments and collects a neat corpus of Rs. 35 lakh at the end of 30 years. On the other hand, Rohit does nothing for 20 years.

He suddenly realizes 10 years before his retirement that he has no savings left for retirement and goes on investing Rs. 12,000 every month for the next 10 years. He also manages to get annual return of 12% on his investments and succeeds in accumulating a corpus of Rs. 27 lakh for his retirement.

So, Pranav got higher returns? Pranav is merely saving Rs. 1,000 every month, while Rohit is investing Rs. 12,000 every month. It's possible because of the time and compounding factor which Pranav has got on his investments.

Apart from the compounding effect, there are a few other factors one should consider while planning for investment: Inflation and Time Value of Money.

A. Inflation

Inflation is one such macroeconomic variable that affects everyone. To define it, inflation refers to a sustained rise in overall price levels of goods and services in an economy over a period of time. It poses a risk to the investors because of rising inflation & decreasing purchasing power. For instance, one opts to invest in savings account and gets 4% interest. The point to note here is whether the investment will be profitable, assuming the inflation rate in the economy is around 6%.

Considering the money deposited in the savings account is Rs. 1,50,000. And interest earned on it is around 4%. The investments at the end of 1 year will work out to be like this:

| S.No | Particulars | Amount |

|---|---|---|

| A | Money invested in savings account | Rs. 1,50,000 |

| B | Interest earned @ 4% in 1 year | Rs. 6,000 |

| C (A+B) | Total value | Rs. 1,56,000 |

| D | Rate of Inflation @ 6% p.a. | Rs. 9,000 |

| E (C–D) | Value of money at the end of year | Rs. 1,47,000 |

To fight inflation, the key is to invest in an option that gives a higher rate of return, which will ultimately help meet long-term goals.

B. Time Value of Money

One of the most fundamental concepts in finance is that money has a time value. That is to say, money in hand today is worth more than money that is expected to be received in the future. Time value of money is dependent not only on the time interval being considered but also the rate of discount used in calculating the current or future values.

Cost of Money Lying Idle

| Particulars | Amount | |

|---|---|---|

| Money in savings account | Rs. 1,00,000/- | |

| Interest earned in 1 year (@4% per annum) | + | Rs. 4,000/- |

| Total value | Rs. 1,04,000/- | |

| Impact of inflation (@5% per annum) | − | Rs. 5,000/- |

| Actual value at the end of year 1 | Rs. 99,000/- |

When Should One Start Investing?

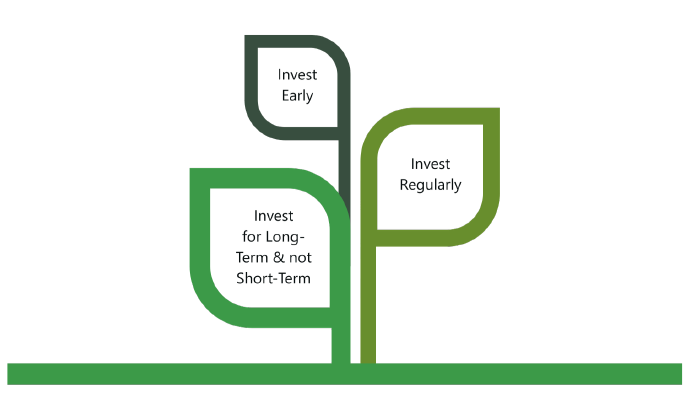

There is no investment duration or age specified for one to start investing. But it is advised: "the earlier one starts, the better", as one can take advantage of compounding returns on their investments.

The three golden rules of investing are as follows:

- Invest Early — Time allows to take risk. It is broadly observed that ones who begin to invest late are more cautious towards their approach. Investing early allows the investor to be open towards investment risks, as they have time on their side which allows the investments to grow.

- Invest Regularly — A disciplined approach of investing allows an investor to exponentially increase returns on investments. Just like the compounding factor allows an investor to reinvest income at the same rate of return which grows along with the initial amount invested. Hence, longer the period on investment, higher the returns accumulated on the investments made. Thereby creating sense why one has to start investing early.

- Invest for Long-Term and Not Short-Term — Investment is a long-term process i.e. the longer one stays invested, the better are the returns on the investment. But how long an investor wants to stay invested depends entirely on how soon an investor would like to use the returns on the investments made.

Key Footsteps to Be Followed While Investing

The following are 12 important steps that an investor should look into before making any investments:

- Obtain the written document explaining the investments in detail.

- Read carefully and understand such offer documents.

- Verify the legitimacy of such investments.

- Find out the cost and other charges associated with the investments.

- Evaluate the risk and return profile of the investments.

- Know the liquidity and safety aspects of the investments.

- Check whether the investments match your specific goals.

- Compare investments with other investment options available.

- Check if the new investment is the best of all considered options and compatible with existing investments.

- Deal only through an authorized intermediary.

- Before investing, seek all clarifications about the intermediary and any investment-related doubts.

- Consider other investment options available; if satisfied, proceed with making investments.

Chapter // 02

Financial Markets

A financial market is a platform that facilitates the exchange of financial instruments. It serves as a place where buyers and sellers come together to trade various assets such as equities, bonds, debentures, currencies, and derivatives.

Financial markets operate through mechanisms that ensure transparency in pricing, basic regulations, transaction costs and fees, and other market forces that help determine the value of securities. These elements allow for fair and efficient pricing, benefiting all participants. The key participants in financial markets include:

- Borrowers — who issue securities to raise funds for various purposes.

- Lenders — who purchase these securities to earn returns.

- Financial intermediaries — who assist and facilitate the trading of securities between borrowers and lenders.

Through these interactions, financial markets enable capital to flow efficiently between those who have funds and those who need them, supporting economic growth and investment.

What Are the Functions of Financial Markets?

The main functions of financial markets are:

- It provides an interaction between investors and borrowers.

- It provides pricing information resulting from trade between buyers and sellers in the market.

- It provides security to dealings in financial assets.

- It provides liquidity by offering a mechanism for an investor to sell financial assets.

- It provides low cost of transactions and information.

Components of Financial Markets

Financial markets are made up of several key segments, each serving a unique purpose in facilitating the flow of capital and managing risk:

-

Capital Markets — These markets help raise long-term funds through:

- Stock markets — enable businesses to raise capital by issuing shares or common stock, while also providing a platform for their subsequent trading.

- Bond markets — allow organisations to secure financing by issuing bonds, which can then be traded among investors.

- Commodity Markets — Provide a platform for buying and selling physical goods like metals, agricultural products, and energy resources.

- Money Markets — Designed for short-term debt instruments, money markets offer avenues for borrowing and lending with maturities of less than one year.

- Derivatives Markets — These markets offer financial contracts such as options and swaps that help investors and businesses manage and hedge against financial risks.

- Futures Markets — Futures markets facilitate trading through standardized forward contracts, allowing participants to agree today on the purchase or sale of products at a specified date in the future.

- Insurance Markets — These markets support the redistribution and management of various risks by offering insurance products that protect against unforeseen events.

- Foreign Exchange (Forex) Markets — Forex markets enable the trading of foreign currencies, assisting in global trade, investment, and currency risk management.

Types of Financial Markets

The Indian financial markets are classified into two types:

a. Money Market

The money market refers to the segment of the financial market where short-term financial assets — which are close substitutes for money — are traded. These instruments typically have a maturity period not exceeding one year and are designed to meet the short-term funding requirements of businesses, governments, and financial institutions.

The instruments traded under these markets are considered as close substitute for money, meaning, a financial asset that can be swiftly and easily converted into cash with minimal transaction costs and without undue effort. This characteristic ensures that participants can access liquidity as needed, enhancing financial efficiency.

Money markets are known for their high liquidity, as securities in this space are traded in large volumes. They play a crucial role in redistributing cash balances in accordance with the liquidity needs of market participants. Common instruments in this market include call money, commercial papers, certificate of deposit, and treasury bills each serving specific purposes within the broader money market framework.

b. Capital Market

A capital market is a marketplace where long-term securities, such as equity and debt instruments, are bought and sold. Its primary objective is to facilitate the raising of capital on a long-term basis — typically over one year — supporting both businesses and governments in financing their growth and development.

These markets serve as a vital platform where public and private entities can offer stakes to investors in exchange for funds.

Capital markets are broadly classified into two segments – the primary market and the secondary market. The primary market is where newly issued securities, like initial public offerings (IPOs), are introduced to investors for the first time. In contrast, the secondary market provides a space where investors can trade existing securities among themselves, ensuring liquidity and efficient price discovery.

Transactions within these markets are distinct in the primary market, interactions occur directly between issuers and investors, whereas in the secondary market, transactions take place among investors themselves. Together, these markets play a critical role in the functioning of modern financial systems by enabling access to capital and investment opportunities.

Money Market vs Capital Market: Key Differences

| Pointers | Money Market | Capital Market |

|---|---|---|

| Definition | Segment of financial market where short-term borrowings take place. | Segment of financial market where long-term borrowings take place. |

| Maturity Period | Less than or up to one year. | More than one year. |

| Financial Instruments | Commercial papers, Treasury bills, Certificate of deposits, etc. | Shares, bonds, debentures, etc. |

| Basic Requirement | Liquidity adjustment | Putting capital to work |

| Risk | Low | High |

| Liquidity | High | Low |

| Return on Investments | Low | Comparatively high |

| Purpose | Short-term credit required for small investments. | Long-term credit required to establish business, expand business or purchase fixed assets. |

Classification of Stocks

Liquidity is a crucial aspect of securities traded in secondary markets. It refers to the ease with which a security can be sold without a loss of value. Securities with an active secondary market have many buyers and sellers at any given time. An illiquid security may force the seller to accept a large discount.

Stocks are classified based on various aspects:

A. On the Basis of Ownership

Common Stock and Preferred Stock

Common stock Common stock represents complete ownership in a company; whereas, preferred stock holders have just partial ownership. Common stock offers more potential over the long-term than any publicly traded investment.

Preferred stock Preferred stocks have fixed amounts paid by way of dividends as they enjoy greater priority at the time of distribution of surplus by the company. These stocks are less risky and therefore, payouts are generally lower than common stocks.

B. On the Basis of Market Capitalisation

Stocks are also classified based on the market capitalization of the company. Market capitalization is calculated by multiplying the share price by the total number of issued shares. Large-Cap stocks, Mid-Cap stocks and Small-Cap stocks are the three main categories of stocks.

These are stocks of companies whose market capitalization is ₹20,000 crore and above. They are well-established, financially strong, and have a significant presence in the market.

These are stocks of companies whose market capitalization is between ₹5,000 crore and ₹20,000 crore. They are medium-sized companies, moderately risky, and offer good growth potential compared to Large-Cap stocks.

These are stocks of companies whose market capitalization is below ₹5,000 crore. They typically include smaller or emerging companies and carry higher risk, but can offer significant growth potential.

📘 Download Full eBook

You can download the complete book in PDF format for offline reading.

Download Full Book (PDF)